When boxing legend Mike Tyson was once asked by a reporter whether he was worried about Evander Holyfield and his fight plan, he answered, “Everybody has a plan until they get punched in the mouth.”

Seconds into round one of their epic 1996 title bout, Tyson threw a ferocious overhand right that sent the “Real Deal” (aka Holyfield) into the ropes. Holyfield overcame this initial fury- and the 15/2 odds- to shock the world and win the heavyweight championship belt.

How did he do it?

Holyfield adapted quickly to deal with the “right now reality” of Tyson’s initial assault by leveraging his superior size and strength to easily walk him into the ropes, keeping Tyson on his heels to negate his punching power. Holyfield adapted but did not totally abandon his original plan.

In many ways, long-term utility planners and grid operators face the same challenge that Holyfield did on that famed evening in Las Vegas. The sudden and unexpected global health pandemic has delivered the right hook to Integrated Resource Plans (IRPs) across the country, in part by triggering unparalleled adjustments in (a) the ways people interact and (b) how the economy is conducted. In aggregate, patterns of electricity use have changed while overall demand has declined.

Adapting: No longer an option.

According to a recent research paper by A.J. Goulding (President, London Economics International LLC), “Potential Implications of The COVID-19 Crisis on Long-Term Electricity Demand In The United States“, the pandemic will likely culminate in a long-term decline in annual electricity utilization by 65.2 TWh to 158.8 TWh, or 1.6% to 4%, reducing the need for baseload generation by 28 GW. It is also likely to hasten changes in the framework of electricity demand that were already underway.

While different regions will experience varied impacts, the Great Lockdown seems destined to present “missing load” challenges to pre-existing long-term utility and RTO forecasts. Like Evander Holyfield, energy market operators and participants will need to adopt new plans to deal with the right now reality while respecting the underlying (and likely accelerating) trends that drove the development of their original plans.

This Time Really Is Different

History truly can help us understand the present and predict the future. To reasonably forecast electricity demand requires a thorough understanding of the present and future status of our economy, which will see a long, difficult climb out of the mire and back to full-functioning.

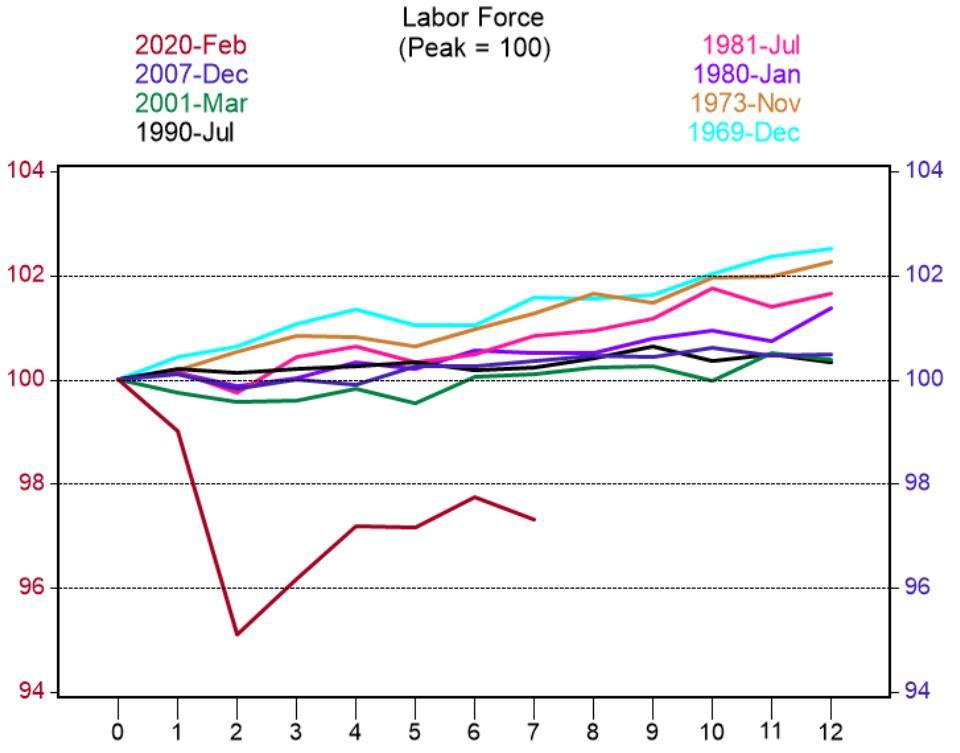

It is appropriate to compare the Great Lockdown to the Great Recession and even the Great Depression. While dozens of statistics measure and describe the economic devastation we’ve experienced, the unemployment rate is one of the most impactful and telling. This country’s COVID-19-related loss of 20.5 million jobs last April was staggering, unprecedented, and, in one month, wiped out all jobs gained since the Great Recession.

Table 1: U.S. Workforce Decline due to COVID-19

Future electricity demand will largely depend on how fast the economy recovers and what activities comprise the growth. And, for those people reentering the labor force, where they work, whether at home or in the office, will also play a significant role in determining electricity demand.

In some ways, the right now reality will be easier to predict in the next six to eighteen months. During the Great Recession, electricity load growth declined in 2008 and 2009 (by 0.6 percent and 3.7 percent, respectively) relative to prior years.

Table 2: Projected Long Term Annual Electricity Demand Impact of COVID-19 Crisis

Load Impact Trends

Underlying

Economic trends predating the Great Lockdown. Some of these trends blossomed anywhere from ten to twenty years ago:

- Number of heating and cooling days: Warming temperatures are generally supportive of load growth due to the increase in cooling days relative to heating days.

- Declining population: Overall, in the post-Great Recession period, the U.S. population has declined, contributing to some missing load.

- Continued transition from manufacturing to services economy: Generally bearish for load growth but somewhat offset by the explosion of data centers.

Table 3: Average Change in Load Growth Factors: 1998-2019

Accelerating

- Increasing materiality of behind-the-meter-generation: A substantial shift in the implementation of distributed energy resources (DERs) is having a significant impact on demand destruction for utilities. Technological advances coupled with a strong incentive to minimize utility bills for a population spending increasing time at home promises additional quantum leaps.

- Improvements in energy efficiency: EIA’s Annual Energy Outlook 2020 (AEO2020) projects that U.S. energy consumption will grow more slowly than gross domestic product (GDP) through 2050 as energy intensity continues its decades-long trend of decline through the AEO2020 forecast period.

- Decline in retail store count and size: Again, Goulding’s report noted that, through 2017-2018, more than 2,200 major stores closed. The U.S. also owns the highest number of GLA (Gross Leasable Area) per capita in the world. This data posits the likelihood that retail space per capita could continue to decline significantly.

- Online shopping: Goulding cites the relationship between retail and logistics demand, with the juggernaut of online shopping driving an increase in demand for warehouse space. That trend can be expected to continue – if not accelerate.

- Transportation: Electric vehicle penetration forecasts from highly respected institutions vary by nearly five times for the next ten years. Transportation accounts for the third largest share (28%) of primary energy in the U.S. and is the least electrified of all sectors.

- Heating electrification: The trend toward more electrified heating is a potentially significant source of demand contingent on the specific technology, weather patterns, evolving demographics, and more.

Why Policy Matters

The old adage is still true: Capital has a funny way of flowing to places where it feels most welcome. State and federal policymakers play a critical role in directing capital using tools such as tax breaks, subsidies, and other incentives to achieve economic growth goals.

At some point, our government will need to develop an economic aid package meant to serve as an economic bulwark for the next decade. The elements of that package, debated daily on social media and almost as frequently in the halls of Congress, could greatly impact the extent of either demand destruction or demand substitution.

“The new normal will look different than the old normal.”

A.J. Goulding argues that, in an era of increasingly difficult load forecasting, regulatory or legislative procurement-related targets should not be denominated in megawatts. Specifically, targets for storage, offshore wind, and other-directed procurements should be expressed as a percentage of load. Further, all targets must be sized accordingly.

Considering the untold dollars in a future economic stimulus package(s), it will be tempting for lobbyists and politicians to toss out politically correct goals, including markers such as “30,000 by 2030”. However, does it make any sense to make statements that include nicely rounded dates and metrics? Do PTC (Production Tax Credits) or ITC (Investment Tax Credits) have any real linkage to actual forecasted needs? Sub-question: Do they have any linkage to the real value of an expected carbon reduction benefit?

Finally, Goulding advocates for continued investment in a smart grid and that it may be among the best uses of potential stimulus spending.

More than ever, long-term energy industry planning must take a 360-degree view of all influencing factors to mitigate risks, including those associated with stranded costs between ratepayers and investors.

Load Profile Changes

Thanks in part to the research of data scientists at the Pacific Northwest National Laboratory, there exists an embryonic understanding of the potential impacts of load profile changes due to long-term structural changes like teleworking. Early studies indicate that it could lead to 5-7% higher spring and summertime peak hourly loads that occur up to 2.5 hours earlier in the day. Such a shift represents a significant challenge for utilities and grid operators to meet their root purpose and duty to provide reliable and affordable electricity supplies for their customers while adhering to an array of evolving energy and environmental regulations and policies.

The total obtained capacity is dependent on peak load forecasts and target reserve margins. Balancing the competing objectives of affordability and reliability has always created a healthy tension in long-term planning. However, amid the backdrop of an unprecedented economic disaster with an alarming number of customers falling behind in their utility payments, forecasters must be hyper-thoughtful in evaluating the procurement of costly – and potentially unnecessary – capacity due to missing load.

Again, with load profile changes varying regionally, energy market stakeholders who share data with each other, as well as authoritative research laboratories and consultants, will overcome critical planning obstacles sooner rather than later.

One thing is for certain:

“The new normal will look different than the old normal.”

Long after his career ended, Mike Tyson explained what he meant when he said, “If you are good, and your plan is working, somewhere during the duration of that, the outcome of that event you are involved in, you’re going to get the wrath, the bad end of the stick. Let’s see how you deal with it. Normally, people don’t deal with it that well.”

Like other important economic sectors, the U.S. energy industry was already challenged by the advent and incorporation of enormously disruptive new technologies when COVID-19 hit. Generally, power providers have responded well, with consumer satisfaction surveys indicating that trust in their local utility to manage the right now reality has increased. Lights have stayed on, and shutoffs have been suspended, allowing millions to stay home and stay safe.

The excellent research cited here by Columbia University indicates a strong possibility that The Great Lockdown will cause future missing load while still pointing out that the possibility may not become a reality. The uncertainty is real and reflects the times we’re navigating through.

On one hand, an economic stimulus package that incents behind-the-meter generation, along with meaningful energy efficiency standards, would further sap load growth. On the other hand, one that focuses on electric vehicles and the electrification of everything would be quite bullish for the load.

“More than ever, long-term energy industry planning must take a 360-degree view of all influencing factors to mitigate risks, including those associated with stranded costs between ratepayers and investors.”

Planners and grid operators are up against the ropes right now in the same way as Holyfield was in the first round against Tyson as they endeavor to successfully adjust to the right now reality and turn their attention to the future challenges that, hopefully, exclude another global pandemic.

If policymakers, planners, and grid operators work very collaboratively, technology and data science can be brought to bear to deliver flexible strategies that provide reliable, affordable energy in the most environmentally considerate manner.

Evander Holyfield defeated Mike Tyson and won the heavyweight championship because he incorporated flexibility in his original plan to survive the opening seconds of the fight. Plans are important, but it’s what you do after you get punched in the mouth that matters most.

Visit our electricity load forecasting software solutions page to learn more.

Sources

“Potential Implications Of The Covid-19 Crisis On Long-Term Electricity Demand”

Columbia University Center On Global Energy Policy

“COVID-19’s Long Term Effects May Cut Need for Baseload Generation”

S&P Global Platts

A.J. Goulding sees potential for drastic permanent demand destruction in the US due to COVID

London Economics

“The Great Lockdown Versus The Great Depression and the 2008 Global Financial Crisis”

Akshat Sogani